A foreign currency exchange market in Baghdad

Recent measures taken by US authorities to tighten the channelling of dollars to Iran from Iraq have decreased the value of the Iraqi dinar on the black market, government officials and traders said on Monday.

The Iran-backed Iraqi government has been struggling to control the exchange rate to contain mounting public anger over soaring goods prices.

The dollar exchange rate in the black market has been hovering around 1,550 Iraqi dinars from around 1,470 dinars, Dhirgham Hameed, owner of a Baghdad-based exchange company, told The National.

“The dinar has been trembling against the dollar since early this month, wreaking havoc in the market,” Mr Hameed, 44, said.

In 2004, the Central Bank of Iraq introduced the foreign currency auction as one of its policy tools to achieve monetary stability.

Through that auction, the government has succeeded in controlling the exchange rate on the black market.

For years, the official rate for banks and exchange companies was 1,182 dinars, while the rate on the street was around 1,200 dinars.

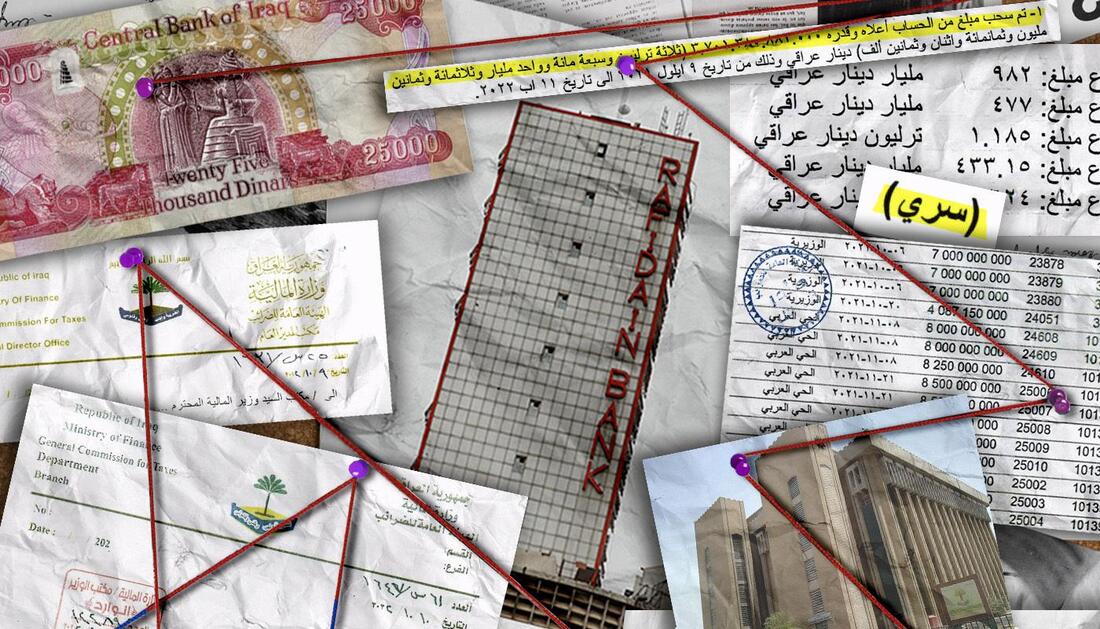

However, the process has been mired with accusations of corruption, money laundering and the channelling of dollars to Iraq’s neighbours, Iran and Syria, using forged bills. Both countries are under punishing US sanctions.

Since then, the US has blacklisted a number of Iraqi banks that deal mainly with Iran. The US sanctioned Iraq's Al Bilad Islamic Bank for dealing with Iran's Islamic Revolutionary Guard Corps in May 2018.

Amid a liquidity crisis due to plummeting oil prices on the international market, Iraq’s Central Bank devalued the dinar in December 2020 to 1,460 dinars per dollar for banks and 1,470 dinars for individuals.

The interim government argued the move would also curb the flight of the “cheap dollar” outside the country.

But that didn’t stop the outflow of much-needed hard currency.

The US Ambassador to Iraq has complained to Iraqi officials on many occasions that the dollar was still being sent to Iran, a Central Bank official and a lawmaker said.

But Mohammed Shia Al Sudani's government, which took office in late October and is close to Iran, has not taken any action, they said.

“When there was no action from the government, the Federal Reserve bank started to apply scrutiny measures on foreign transactions and that has delayed the process of releasing the money from the US to cover the imports and other needs,” the Central Bank official said.

Both spoke on condition of anonymity as there is no government statement on the latest US measures.

The Iran-backed Iraqi government has been struggling to control the exchange rate to contain mounting public anger over soaring goods prices.

The dollar exchange rate in the black market has been hovering around 1,550 Iraqi dinars from around 1,470 dinars, Dhirgham Hameed, owner of a Baghdad-based exchange company, told The National.

“The dinar has been trembling against the dollar since early this month, wreaking havoc in the market,” Mr Hameed, 44, said.

In 2004, the Central Bank of Iraq introduced the foreign currency auction as one of its policy tools to achieve monetary stability.

Through that auction, the government has succeeded in controlling the exchange rate on the black market.

For years, the official rate for banks and exchange companies was 1,182 dinars, while the rate on the street was around 1,200 dinars.

However, the process has been mired with accusations of corruption, money laundering and the channelling of dollars to Iraq’s neighbours, Iran and Syria, using forged bills. Both countries are under punishing US sanctions.

Since then, the US has blacklisted a number of Iraqi banks that deal mainly with Iran. The US sanctioned Iraq's Al Bilad Islamic Bank for dealing with Iran's Islamic Revolutionary Guard Corps in May 2018.

Amid a liquidity crisis due to plummeting oil prices on the international market, Iraq’s Central Bank devalued the dinar in December 2020 to 1,460 dinars per dollar for banks and 1,470 dinars for individuals.

The interim government argued the move would also curb the flight of the “cheap dollar” outside the country.

But that didn’t stop the outflow of much-needed hard currency.

The US Ambassador to Iraq has complained to Iraqi officials on many occasions that the dollar was still being sent to Iran, a Central Bank official and a lawmaker said.

But Mohammed Shia Al Sudani's government, which took office in late October and is close to Iran, has not taken any action, they said.

“When there was no action from the government, the Federal Reserve bank started to apply scrutiny measures on foreign transactions and that has delayed the process of releasing the money from the US to cover the imports and other needs,” the Central Bank official said.

Both spoke on condition of anonymity as there is no government statement on the latest US measures.

How the process goes

Each dollar Iraq gains from selling crude oil goes to an account at the Federal Reserve Bank of New York, and Iraq makes withdrawals to pay government salaries and imports.

Oil revenue makes up nearly 95 per cent of the federal budget and the war-torn country depends heavily on imports to meet the demand for food and materials for key sectors of the economy.

The Federal Reserve Bank of New York supplies Iraq with hard currency on request from the Iraqi government, either in cash or foreign transactions.

While some of these funds are used to cover government imports and other requirements, much of it is passed on to commercial banks, ostensibly for private sector imports in a process that was hijacked long ago by Iraq’s money-laundering cartels.

The rest of the money is added to the international reserve.

Thanks to Iraq’s growing oil revenue, the Central Bank of Iraq has about $96 billion in foreign exchange reserves, Mr Al Sudani announced early this month.

As of last month, the CBI sold an average of $240 million to $250 million a day, said another owner of an exchange company, who asked to remain anonymous.

Only 10 per cent to 20 per cent of the money was cashed out to be distributed to banks and exchange companies and then to individuals, while the rest was sent to accounts in Dubai, Turkey, Amman and China to cover private sector imports, he said.

“Iraq has no problem with the money at all, it has good reserves,” the exchange company owner said. “It sounds as if the issue is politically motivated because the Americans are upset.”

Over the past 19 years, the Federal Reserve has never delayed a request or transaction from Iraq, he said. “They used to approve any bill immediately,” he added.

“But since early this month, the Americans have started applying scrutiny measures on foreign transactions and the new process has delayed each transaction for up to two weeks,” the exchange company owner said.

He added that most of the requests were being rejected due to suspicions that some banks are linked to Iran.

Since then, daily transactions have dropped from around $200 million to between $20 and $30 million a day.

“The reserves have been dried up in the accounts abroad and that has pushed up the demand for the dollar in the local market to cover imports,” he said.

To control the rate at the black market, the government has asked the CBI to take urgent steps to compensate for a dollar shortage in the local market.

It reduced the exchange rate for individuals from 1,470 dinars to 1,465 dinars to cover travel for the Hajj pilgrimage, medical treatment and study.

It also asked the CBI to help private banks strengthen their non-US dollar foreign currency reserves such as the Chinese yuan, the euro, the Emirati dirham and the Jordanian dinar.

But these measures failed to strengthen the currency.

“We are not optimistic and we believe that the worst is yet to come unless the government applies urgent, immediate and effective measures,” Mr Hameed said.

The current official dinar to dollar exchange rate is 158,000.

Each dollar Iraq gains from selling crude oil goes to an account at the Federal Reserve Bank of New York, and Iraq makes withdrawals to pay government salaries and imports.

Oil revenue makes up nearly 95 per cent of the federal budget and the war-torn country depends heavily on imports to meet the demand for food and materials for key sectors of the economy.

The Federal Reserve Bank of New York supplies Iraq with hard currency on request from the Iraqi government, either in cash or foreign transactions.

While some of these funds are used to cover government imports and other requirements, much of it is passed on to commercial banks, ostensibly for private sector imports in a process that was hijacked long ago by Iraq’s money-laundering cartels.

The rest of the money is added to the international reserve.

Thanks to Iraq’s growing oil revenue, the Central Bank of Iraq has about $96 billion in foreign exchange reserves, Mr Al Sudani announced early this month.

As of last month, the CBI sold an average of $240 million to $250 million a day, said another owner of an exchange company, who asked to remain anonymous.

Only 10 per cent to 20 per cent of the money was cashed out to be distributed to banks and exchange companies and then to individuals, while the rest was sent to accounts in Dubai, Turkey, Amman and China to cover private sector imports, he said.

“Iraq has no problem with the money at all, it has good reserves,” the exchange company owner said. “It sounds as if the issue is politically motivated because the Americans are upset.”

Over the past 19 years, the Federal Reserve has never delayed a request or transaction from Iraq, he said. “They used to approve any bill immediately,” he added.

“But since early this month, the Americans have started applying scrutiny measures on foreign transactions and the new process has delayed each transaction for up to two weeks,” the exchange company owner said.

He added that most of the requests were being rejected due to suspicions that some banks are linked to Iran.

Since then, daily transactions have dropped from around $200 million to between $20 and $30 million a day.

“The reserves have been dried up in the accounts abroad and that has pushed up the demand for the dollar in the local market to cover imports,” he said.

To control the rate at the black market, the government has asked the CBI to take urgent steps to compensate for a dollar shortage in the local market.

It reduced the exchange rate for individuals from 1,470 dinars to 1,465 dinars to cover travel for the Hajj pilgrimage, medical treatment and study.

It also asked the CBI to help private banks strengthen their non-US dollar foreign currency reserves such as the Chinese yuan, the euro, the Emirati dirham and the Jordanian dinar.

But these measures failed to strengthen the currency.

“We are not optimistic and we believe that the worst is yet to come unless the government applies urgent, immediate and effective measures,” Mr Hameed said.

The current official dinar to dollar exchange rate is 158,000.

RSS Feed

RSS Feed